Okay, let’s talk HDFC Bank. As someone who’s been following Indian stocks for a while, I’ve always considered HDFC Bank a pretty solid player. It’s the kind of stock you could almost set and forget (at least till 4-5 years back). But lately, something’s been off. I noticed its P/E ratio is bumping along at its lowest level in a decade, and it’s got me digging into what’s going on.

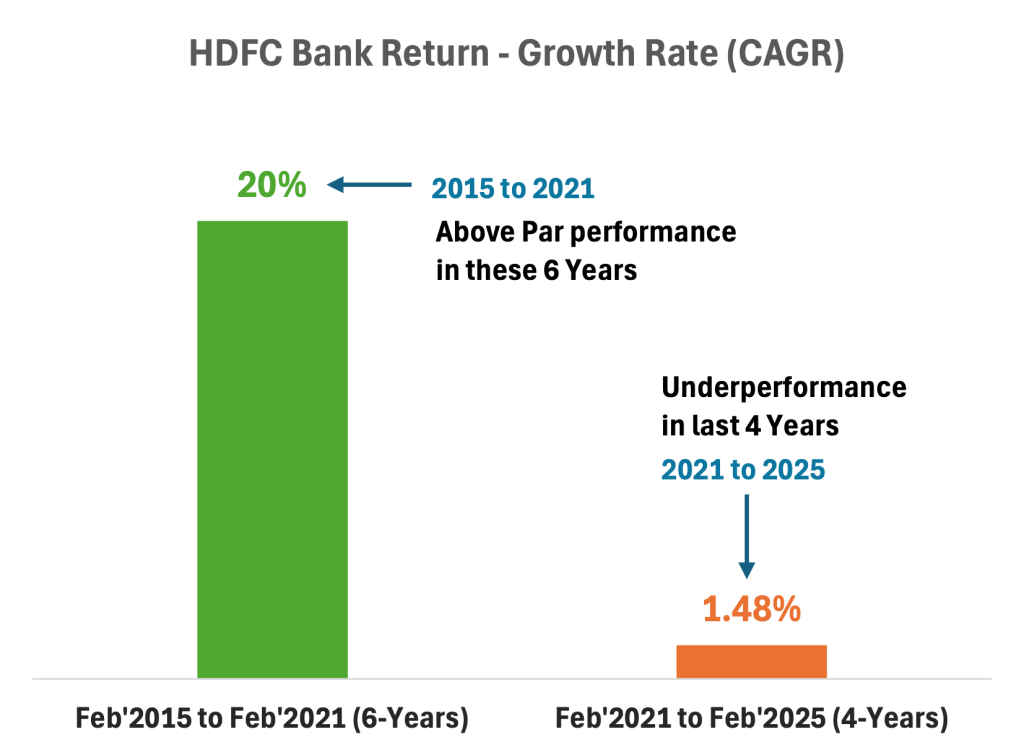

It wasn’t always like this, right? I remember those years between 2015 and 2021. The stock was on fire, delivering returns of around 20% CAGR growth. It felt like a sure thing. But then, things cooled down. Since 2021, it’s been inching along, growing at just a fraction of that previous pace, about 1.5% annually. What changed?

1. What Changes With HDFC Bank?

Well, the elephant in the room is the HDFC Ltd. merger in July 2023.

This wasn’t just some small acquisition; it was a massive shakeup. It created a colossus in the financial world, sure. But it also threw a whole bunch of new variables into the equation.

On the one hand, it makes perfect sense. Imagine, the merged group is now being able to offer mortgages to every HDFC Bank customer. Moreover, every HDFC Ltd’s home loan borrower will now get all banking services. The potential for growth and cross-selling is immense. Plus, you’d expect some serious cost savings as they streamline their operations.

But here’s where things get a bit trickier.

Merging two giants like that? It’s like trying to combine two entirely different cities. You’ve got different systems, different ways of doing things, and, let’s be honest, different corporate cultures. It’s going to take time and effort to get everything running smoothly. While this transition is getting streamlined, there are bound to be a few bumps along the way.

2. Significant Changes in HDFC Bank Post Merger

The sheer size of the new merged entity is the biggest challenge.

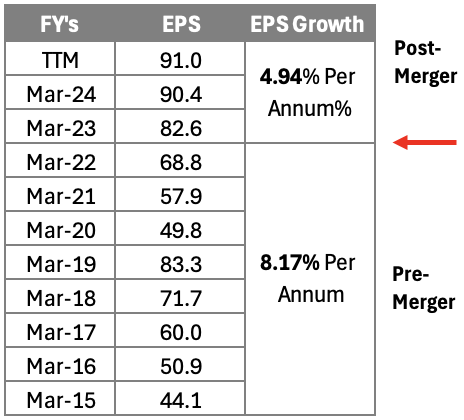

2.1. Earnings Per Share (EPS)

All those new shares issued as part of the merger mean that even if profits go up, earnings per share (EPS) might not climb as quickly as they used to. That directly impacts how investors value the stock. The merger happened in Year 2023. Till 2023, HDFC Bank’s EPS grew at a CAGR of 8.17% per annum. Post merger, EPS growth slowed down to 4.94% per annum.

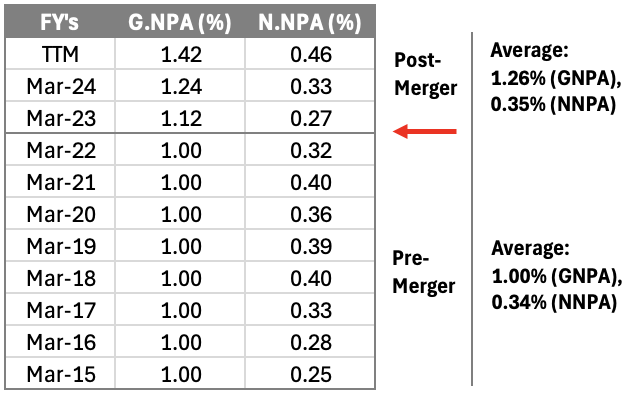

2.2. Non Performing Assets (NPAs)

And I’m not going to lie, I’m keeping a close eye on asset quality. Bringing HDFC Ltd.’s massive mortgage portfolio into the mix means there’s more exposure to the housing market. We all know how stubborn real estate can be, and I want to see how HDFC Bank manages those risks. I noticed a slight uptick in average Gross NPA and Net NPA from 1% and 0.34% to 1.26% and 0.35% respectively (between pre-merger and post-merger). It’s not a crisis, but it’s something to watch.

Though, what’s worth watching is Net NPA jumping from 0.33 to 0.46 (in 9 Months – Between Mar’24 and Dec’24 quarters)

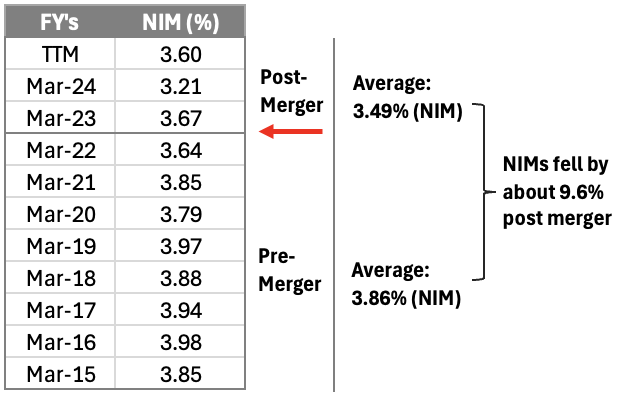

2.3. Net Interest Margin (NIM)

NIMs has fluctuated between 3.60% to 3.98% in the last 10-Years, which is not so bad. But what is more concerning for the investors is gradually fall in the NIMs from 2020 till date. In this period, there was also the merger in 2023. Before the merger, the average NIMs of HDFC Bank was about 3.86%. Post, merger, it fell to a 3-Year average of 3.49%. Looking at average NIMs, post the merger, the NIM has contracted by about 9.6% after the merger. But, we cannot ignore the jump in NIMs between Mar-24 and TTM (from 3.21% to 3.6%). Is the NIMs rising trend back? This is the real question.

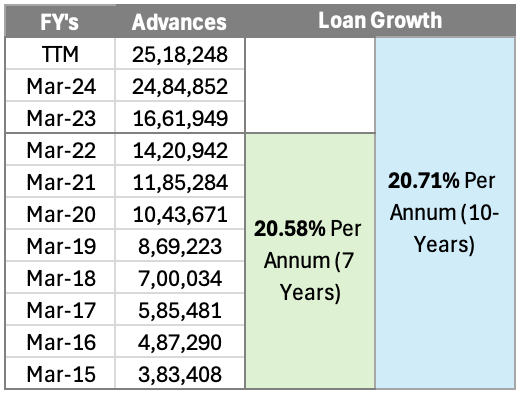

2.4. Loan Book (Advances)

One clear thing that we can make out from the past numbers is that HBFC bank is doing good business. The advances have grown significantly from 3,83,408 to 25,18,248 crores in 10-years. This is a CAGR of 20.71%. Before the merger (between 2015 and 2022), the loan book was growing almost at a similar pace of 20.58% per annum. So, one thing is for sure, the core business of HDFC Bank (lending money) is still growing at an impressive pace.

3. Let’s Look At The Macroeconomic Data & HDFC Bank’s Peers

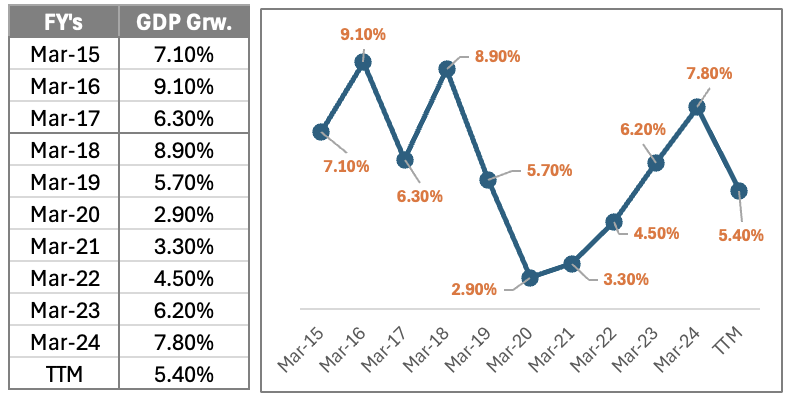

Okay, we all know the economy is a massive beast with tons of moving parts. But for a bank like HDFC Bank, two numbers are particularly important to understand in order to derive future prospects: GDP growth and the RBI’s repo rate. Right now, they’re telling a story that’s part opportunity, part caution.

3.1 GDP Growth

Let’s rewind a bit. Looking back at the GDP growth figures over the past decade, you see a rollercoaster. We had some really strong years, above 7% growth in many cases. But then came the pandemic, and things took a nosedive. Now, we’re in a recovery phase, but the question is: how sustainable is it?

The data show a decline in GDP growth from 7.8% to 5.4% in a single year, and while that’s still growth, it’s a significant deceleration. But we must also remember that Year 2024 was a year of Nation Election in India where government spending (CAPEX) ceases to almost zero. In 2025 onwards, the spending is likely to start again. This will also encourage private CAPEX to show momentum.

Now, what does this trend mean for HDFC Bank?

Consider this, If the economy is booming, businesses are expanding, and people are buying houses and cars. All of that requires credit. Strong GDP growth translates directly into higher loan demand. In turn, loan demand means higher profits for banks.

But if growth starts to sputter, that loan demand could weaken. And, more worryingly, existing borrowers might struggle to repay their loans. Banks are the first victim in an economic slowdown.

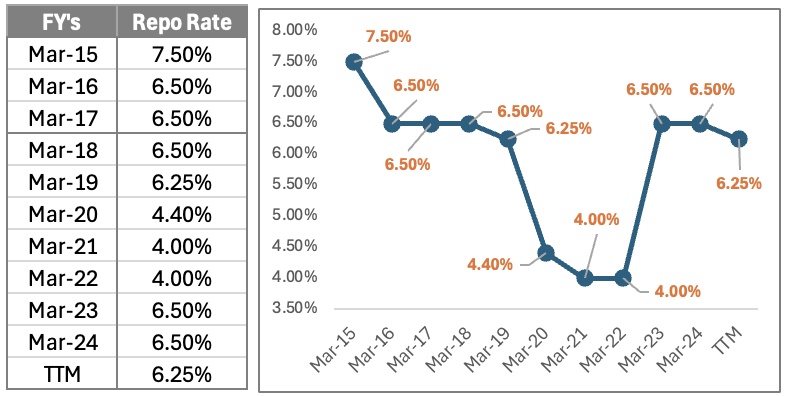

The Repo Rate

The RBI’s repo rate is another critical piece of the puzzle. It’s the rate at which the central bank lends money to commercial banks, so it essentially sets the baseline for borrowing costs in the entire economy. As of today, it stands at 6.25%.

In general, a higher repo rate tends to cool down the economy because borrowing becomes more expensive. That can help control inflation. But it can also put a damper on loan growth. A lower repo rate, on the other hand, can stimulate the economy by making borrowing cheaper.

The RBI is walking a tightrope because they are balancing between controlling inflation and growing the economy.

While 6.25% provides a good number to facilitate both objectives, but what’s evident from the past trends, the repo rate below 6% is what will be necessary to push the GDP growth rate close to 7% in next couple of years. The trend of falling repo rate has also started. This is a good signal for shareholders of strong banks like HDFC Bank.

Are HDFC Bank Shares Really Cheap?

Let’s compare HDFC Bank’s valuation multiples to its main competitors: ICICI Bank and Axis Bank. This is where it gets interesting.

| Valuation of Peers | Current (P/E) | Current (P/B) | Dividend Yield (%) |

| HDFC Bank | 18.63 | 2.76 | 1.15 |

| ICICI Bank | 17.71 | 5.67 | 0.79 |

| Axis Bank | 10.96 | 2.59 | 0.1 |

On the surface, HDFC Bank’s P/E ratio is somewhat closer to its peers. But the Price-to-Book (P/B) ratio tells a very different story. While ICICI Bank is trading at a much higher P/B, HDFC Bank is much closer to Axis bank which could potentially be concerning.

That higher P/B ratio suggests that investors are willing to pay a premium for ICICI Bank’s assets, implying stronger confidence in its future prospects.

So why is HDFC Bank trading at a lower P/B multiple?

- Merger Uncertainty: The market may still be uncertain about the long-term impact of the HDFC Ltd. merger. Investors might be waiting to see how well the integration goes before fully revaluing the stock.

- Asset Quality Concerns: As we discussed earlier, there are some concerns about the asset quality of the combined entity, particularly in the housing loan portfolio. If investors believe that HDFC Bank is carrying more risk on its balance sheet, they may be less willing to pay a premium for its assets.

- Growth Expectations: The market might simply have lower growth expectations for HDFC Bank compared to ICICI Bank. Perhaps investors believe that ICICI Bank is better positioned to capitalize on future growth opportunities in the Indian banking sector.

Let’s not forget that the dividend yield of HDFC Bank is higher than its peers. As investors look at HDFC Bank’s financial statements, they see more risk to the stock given that it is going through an integration. In that case, investors would need to be compensated for the risk, either in the form of increase in prices of the shares or dividend yield.

Conclusion

So, what’s the takeaway?

The current macroeconomic environment presents both opportunities and challenges for HDFC Bank. While India’s long-term growth story remains intact, the recent slowdown in GDP growth and the RBI’s balancing act with the repo rate create some uncertainty in the near term.

The valuation multiples, when compared to peers, shows that the market is waiting for the post merger effects to play out and give the green signal on the stock.

For long-term investors, HDFC Bank could still be a worthwhile investment.

The management needs to show that the long term strategy has been achieved through this merger. If the management can convey the same to the investor, there may be a possibility of the stock doing good. If the investor is confident in this long-term view, the current valuation can be said as potentially attractive.

So, where does all this leave us? Is HDFC Bank a screaming buy, a hold, or a sell?

For me, someone who’s thinking about the next 10 to 15 years and is not worried about the performance of share in next 1-2 years, HDFC Bank is perhaps the most undervalued stocks in the Nifty 50 basket (considering risk-rewards balance).

Moreover, at present the FIIs are exiting the Indian market, but they will come back (their USA story is not going to continue for too long). When FIIs will start investing back in the Emerging Markets, in India they will mainly buy stocks from the Nifty 100 basket. In this basket, they will see HDFC Bank as one of the most undervalued stock.

Have a happy investing.