There has been a rollercoaster ride happening in Polycab stock. Since mid-December 2024, its share price has corrected by a hefty 33.7%. That’s big correction, right? And to top it off, there’s this buzzing news about UltraTech stepping into the wires and cables game, scaring existing investors in the wire and cables businesses. If you’re holding Polycab shares, you might be wondering, “Should I bail out now?” And if you’re sitting on the sidelines, you’re probably asking, “Is this dip a golden opportunity, or a trap?” Let’s discuss these points in this blog post.

I’ve been digging into Polycab’s latest corporate presentation , and I’ve got some thoughts to share. My idea of reading this report was to understand how deep are the fundamental of Polycab to take on new threat of UltraTech. This post isn’t just about numbers, it’s about figuring out what’s practical for us as investors in this chaotic market.

So, allow me to declutter the Polycab space, step-by-step, and see if we can make sense of whether it is still worth our time and money.

What’s Happening with Polycab?

First off, let’s talk about that 33.7% correction.

It’s not just Polycab, India’s broader market has been wobbly since September 2024. Since these last 6 months or so, the Nifty50 index has corrected by about 14%. A lot of stocks have taken a hit.

But then UltraTech also dropped a bombshell. They’re venturing into the wires and cables sector with a Rs.1,800 crore investment.

If that sounds familiar, it’s because it echoes what happened in the paint industry when Birla Opus (another Aditya Birla Group venture) stormed in and shook up giants like Asian Paints.

Naturally, Polycab investors are spooked. Is UltraTech about to pull a similar stunt here?

If you’re holding Polycab, you might be sweating, wondering if this is the beginning of the end. And if you’re thinking of buying, that 33.7% discount looks tempting, but is it a value buy or a value trap?

Before we jump to conclusions, let’s zoom into Polycab’s story and see what’s under the hood.

Polycab’s Strengths

Why it’s not just another stock?

Alright, so I flipped open that presentation and saw what Polycab’s got going for it. For sure, it’s not a lightweight player.

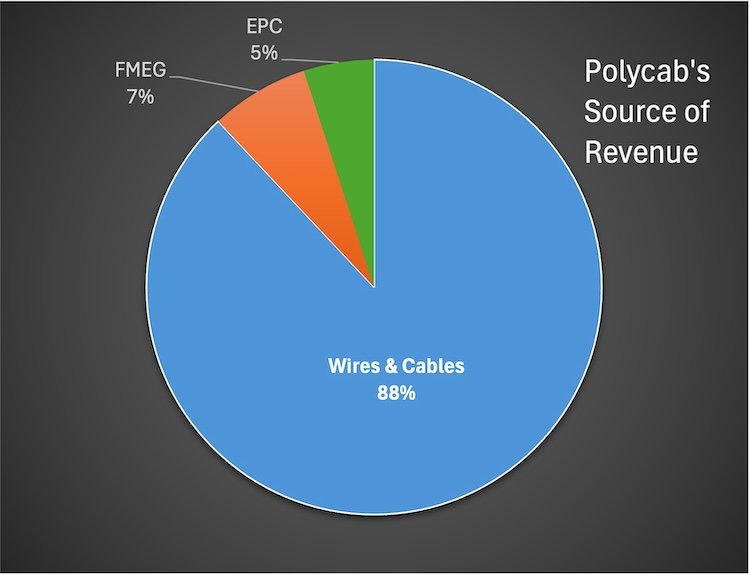

They’re the biggest player in the wires and cables space. Polycab’s 88% of their FY24 revenue was from this segment. Another 7% from Fast-Moving Electrical Goods (FMEG) and 5% from other stuff like EPC projects.

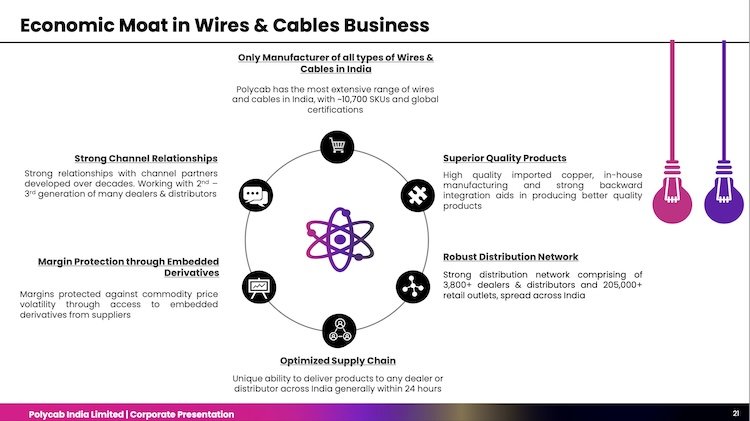

They’ve been at it for decades, building a rock-solid reputation and a distribution network that spans over 4,300 authorized distributors and 2 lakh retail outlets. That’s not something a new entrant can replicate overnight, not even if you’re UltraTech with deep pockets.

Then there’s the Fast-Moving Electrical Goods (FMEG) segment. They have fans, switches, and lighting, which makes up 7% of sales but is growing at a fast 25% CAGR over the last eight years, outpacing many peers.

The rest (5%) comes from stuff like EPC projects.

What’s the takeaway here? Polycab isn’t a one-trick pony. They’ve got a diversified portfolio, and they’re playing it smart.

The Growth Drivers

Now, let’s talk growth drivers.

The Indian cable and wire industry, is projected to grow at 1.5-2x GDP, hitting Rs.1,150 billion by FY27 with a 9% CAGR.

The presentation paints a rosy picture for the Indian cable and wire industry, projected to grow from Rs.800 billion in FY24 to Rs.1,150 billion by FY27E at a ~9% CAGR, riding the wave of 1.5-2x GDP growth. Why? Because India’s infrastructure is booming, government projects, energy transitions, real estate upcycles, and sunrise sectors like EVs and data centers are fueling demand.

Polycab’s sitting strong to cash in on this wave.

Financials

The financials of Polycab are solid.

In the presentation, the company shows revenue, EBITDA, and PAT trending upward impressively over the years.

- Revenue has climbed steadily from Rs.79,856 million in FY19 to a robust Rs.1,41,078 million in FY24, boasting an 18% CAGR, reflecting strong top-line growth.

- EBITDA has surged from Rs.9,504 million in FY19 to Rs.24,918 million in FY24, with a 21% CAGR and EBITDA margin too improving from 11.9% to 13.8%. It is a clear indication of operational efficiency gains.

- Profit After Tax (PAT) has also soared from Rs.5,003 million in FY19 to Rs.18,029 million in FY24, with a 29% CAGR and PAT margins rising from 6.3% to 10.0%. It displayes Polycab’s ability to boost profitability.

These consistent upward trajectory across key metrics is a proof of their financial muscle and growth potential.

Debt, Capex, and Dividends

They’re nearly debt-free, with a net cash position, and they’ve been pumping money into capex (Rs.6,000-8,000 crore planned, all from internal funds), no loans needed.

Plus, they’ve distributed out Rs.12.5 billion in dividends since listing five years ago, with a market cap growing at a 46% CAGR.

That’s a company, I’ll say confidently, that knows how to reward shareholders while keeping the growth engine humming.

The UltraTech Threat

Okay, let’s tackle the elephant in the room, UltraTech.

When they announced their entry, Polycab’s stock got hammered, along with peers like KEI Industries and RR Kabel, losing crores in market cap in a single day.

Investors are freaking out, thinking UltraTech’s muscle (brand, distribution, and cash) could squeeze Polycab’s margins or steal market share. Sound familiar? It’s the Asian Paints vs. Birla Opus playbook all over again.

But hold up, let’s not hit the panic button just yet. UltraTech’s Rs.1,800 crore facility in Gujarat won’t be operational until December 2026. That’s almost two years away. Even then, analysts like Nuvama estimate that with 60-70% capacity utilization by year three, UltraTech might snag less than 5% of the market by FY28.

Compare that to Polycab’s current dominance, 19% market share in cables and wires, and it’s clear they’re not going down without a fight.

Here’s another angle, the wires and cables market isn’t like paints. Paints is an oligopoly, dominated by a few big names, while cables and wires are more fragmented.

The presentation (PPT) lays it out, the global cables and wires market is a massive $250 billion, growing at a 7.5%+ CAGR, with India’s slice at Rs.84,500 crore in FY24. There’s room for multiple players, especially since 70% of the Indian market is organized, and the shift from unorganized to organized players (boosted by GST and safety norms) actually favors established names like Polycab.

UltraTech might have an edge in sourcing raw materials (copper and aluminum) through Hindalco, another Aditya Birla company, and their 4,500 UltraTech Building Solutions stores could fast-track their wire sales in the housing segment. But cables, the B2B side that’s 65-70% of Polycab’s mix, require approvals, tenders, and long-term contracts.

That’s a tougher nut to crack, even for a giant like UltraTech.

The Asian Paints Parallel

When Birla Opus entered the paint market, Asian Paints took a hit, its stock corrected, margins got squeezed, and growth slowed as competition heated up.

Could Polycab face the same fate?

Maybe, but there are differences. Asian Paints was in a mature, consolidated market where new entrants could disrupt pricing fast. Wires and cables, though, are tied to infrastructure and industrial demand, sectors with stickier contracts and higher entry barriers.

Polycab’s economic moat is another ace up its sleeve, brand loyalty, a massive distribution network, and manufacturing scale (25 facilities across India). UltraTech will need years to build that kind of trust and reach. Plus, Polycab’s not sitting still, they’re expanding capacity and eyeing exports (a $250 billion global opportunity) to stay ahead.

So, Should You Hold or Sell?

If you’re a Polycab shareholder, here’s my two cents, don’t let the UltraTech news scare you into a rash exit. That 33.7% drop stings, no doubt, but Polycab’s fundamentals haven’t changed overnight.

The industry’s growth story is intact, ₹9 trillion in power T&D investments over the next seven years, real estate expected to balloon from $200 billion in 2021 to $1 trillion by 2030 at a 19.5% CAGR, and sunrise sectors like EVs and data centers taking off.

Polycab’s got a front-row seat to all of it.

The stock’s now trading at a more reasonable valuation, say, 35x FY26 PE (estimation). This PE multiple is down from loftier levels before the correction. If you’re in for the long haul (think 3-5 years), this could be a dip worth riding out.

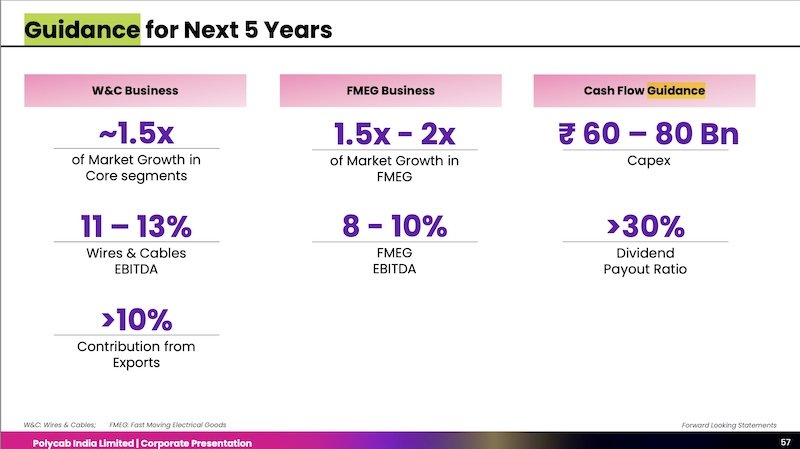

In the presentation, where there’s Polycab’s guidance for the next five years gives confidence, double-digit growth, healthy margins, and a focus on sustainability.

Plus, that near-debt-free balance sheet means they’ve got the firepower to weather any storm.

But here’s the risk, if UltraTech plays dirty with aggressive pricing (like Birla Opus did in paints), margins could take a hit in the medium term. Keep an eye on Polycab’s Q4 FY25 results (due soon) and watch for any signs of pricing pressure or market share loss.

If you’re risk-averse like some of my senior citizen readers, maybe trim your position, but I wouldn’t dump it all just yet. Of-course, this is what I’ll do, but you must take your own call based on your risk appetite.

Should You Buy the Dip?

Now, if you’re a new investor thinking 33.7% correction from peak is juicy, here’s the deal, it’s tempting, but don’t dive in blind.

Polycab’s still a quality stock, it has a leadership in a growing industry. It also has a strong financials:

- ROCE: In FY19, its ROCE was 27.9%, and now in FY24, it has increased to 29.6%.

- ROE: In FY19, its ROCE was 17.5%, and now in FY24, it has increased to 22.6%.

At 35x FY26 PE, it’s not dirt-cheap, but it’s not crazy expensive either, given the growth runway.

The UltraTech risk is real, but it’s not immediate. You’ve got a two-year buffer before their plant even fires up, and Polycab’s got time to fortify its defenses. Plus, there is a latest news dated 13-Mar-25 mentioning a ₹3,003 crore order from BSNL, is a proof that Polycab is still winning big contracts.

If you’re okay with some short-term volatility and believe in India’s infra boom, this could be a smart entry point (I think it this way, you must apply your own rationale).

Had I been a fresh investor in Polycab, I’ll Start small, average down if it dips more, and keep some cash handy for surprises.

Conclusion

For me, investing isn’t about knee-jerk reactions, it’s about seeing the forest for the trees.

Polycab’s taken a beating, no question, and UltraTech’s entry adds a twist to the plot. But this isn’t a sinking ship.

The wires and cables sector is buzzing with opportunity, and Polycab’s got the business to stay in the game, brand, scale, and financial muscle.

For holders, I’ll say hang tight unless you see red flags in the next earnings report. For buyers, I” say dip your toes in if you’re ready for a bit of volatility with a solid payoff down the road (in long-term 5-7 years).

[Note: Surely, it’s not an investment advice but just sharing my thoughts on what I’m thinking presently.]

Either way, keep your eyes peeled and your emotions in check. Markets love to test our patience, but the smart investors have it in them to stay cool and play the long waiting game.

What do you think? Are you sticking with Polycab or eyeing the exit?

Drop your thoughts in the comment section below. I’d love to hear what you are thinking about this stock.

Have a happy investing.