Summary Points:

- L&T will build new offshore platforms in Qatar’s North Field to boost gas pressure, supporting LNG production growth from 77 to 142 million tonnes by 2030.

- The project involves engineering, fabricating, and installing compression complexes, power generators, flare systems, and bridges, integrating with existing infrastructure.

- With a 12% profit margin, L&T could earn Rs. 360 crore annually, adding Rs. 2.62 to its EPS (from Rs. 99), a 2.6% boost.

- This deal strengthens L&T’s global presence, order book (Rs. 4,70,000 crore), and financial stability, potentially driving EPS to Rs. 140-150 by 2030.

Introduction

Larsen & Toubro (L&T) has bagged a massive contract from QatarEnergy LNG. This deal is being called the largest single contract L&T has ever landed, valued at over a billion, roughly Rs. 15,000 crore (order value has not been made public by L&T). As L&T has categorized this project as Ultra-Mega project, its order value will be certainly over Rs.15,000 crore (check this L&T page for details).

The scale of this order is huge? We’re talking about a project that’s going to keep L&T busy until 2030. This project will all happening 80 km off the shores of Qatar in the Persian Gulf. As an Indian, I feel a bit proud, that our very own L&T has got such a massive contract.

So, I thought, why not dig into this a little deeper and share what it’s all about with you?

I’ll share with you the details of what exactly is L&T doing in this “North Field Production Sustainability Offshore Compression Project (NFPS COMP 4)“. After discussing the engineering scope side of the project. I’ll also talk about how’s it’s going to impact their earnings of L&T in the years ahead?

What’s L&T’s Score of Job in The Qatar Project?

Qatar has this massive underwater gas field called the North Field. It is the biggest of its kind in the world.

They’ve been pulling out natural gas from there for years to make LNG. This LNG they cool down to ship worldwide.

But there is an issue with these natural resources, over time, the pressure in these gas fields drop. It’s like when you’re blowing air out of a balloon; at first, it’s easy, but after a while, you need to apply some pressure to squeeze out all air.

QatarEnergy wants to keep the gas flowing strong, and that’s where this L&T contract comes into picture.

L&T Scope of Work

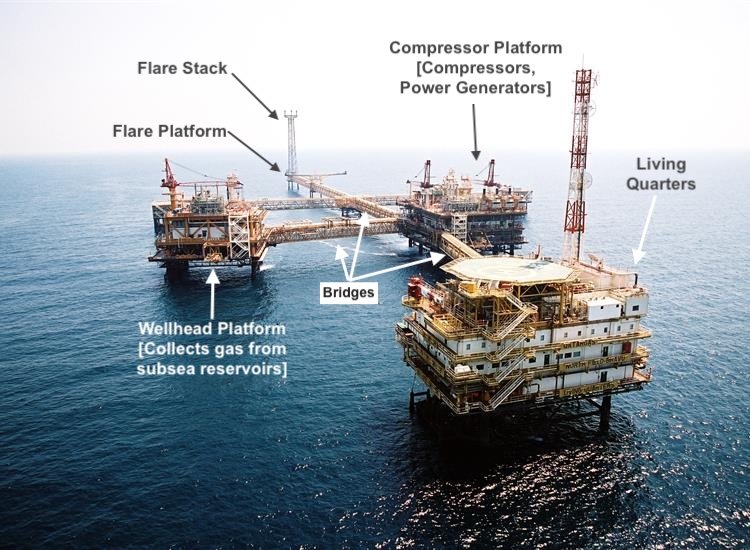

The above image is of the existing offshore platforms in the North Field, Qatar’s massive gas field. It was likely built in earlier phases back in the 2000s or 2010s. The North Field has been producing gas for many years now, and these setups are probably from projects like North Field Alpha, designed to extract and process gas long before the current expansion plans kicked in.

What will be the L&T’s role in the North Field Production Sustainability Offshore Compression Project (NFPS COMP 4)?

But with the field’s reservoir pressure dropping over time, QatarEnergy is now focusing on sustainability and boosting production and hence gave the contract to L&T

I think, L&T’s job will be to build new offshore platforms, not modify the ones in the image. They’re tasked with engineering, fabricating, and installing fresh compression complexes. Imagine new steel platforms with compressors, power generators, flare systems, and bridges right adjacent to the existing facility. While L&T’s platforms will be new, they’ll connect to the North Field’s existing network, possibly tying into older platforms like the ones in the image via pipelines, ensuring the gas keeps flowing smoothly to shore.

It’s a massive undertaking, and I’m excited to see how L&T pulls it off.

These new setups will boost the declining gas pressure and help Qatar increase its LNG production from 77 million tonnes per year to 142 million by 2030.

How Will This Rs. 15,000 Crore Deal Affect L&T’s Earnings?

How’s this going to hit L&T’s profits and earnings per share (EPS)?

I know, you love numbers when it comes to business (stocks), so let’s do some quick math and see what we can find.

First off, I’m assuming that the contract’s worth Rs. 15,000 crore. It’s supposed to be commissioned by 2030. That’s about 5 years from now (2025). So, roughly, L&T could be billing and collecting about Rs.3,000 crore per year from this project.

But not all of that is profit.

In engineering and construction projects like this, profit margins are usually decent but not crazy high. For offshore oil and gas contracts, margins typically hover around 10-15%. Let’s assume L&T gets a solid 12% margin, it sounds reasonable for a project this big and complex.

So, 12% of Rs. 15,000 crore is Rs.1,800 crore (in five years). That’s the total net profit L&T could make over the 5 years. Spread it out, and we’re looking at Rs. 360 crore of extra profit each year from this North Field.

But how does that effect the EPS of L&T. I’m more interested in that.

- The currently EPS of L&T is about Rs. 99 per share.

- L&T has about 137.47 crore shares outstanding.

- To find the EPS boost, we divide the yearly profit by the number of shares:

- Rs. 360 crore ÷ 137.47 crore shares = Rs. 2.62 per share.

So, this contract could add Rs. 2.62 to L&T’s EPS each year, taking it from Rs. 99 to around Rs. 101.62. It’s just a nice little bump of about 2.6%. Imagine, an Ultra-Mega project like this can add only about 2.6% to its bottom line each year.

It’s not a massive jump, but here’s why it matters. L&T’s already a giant, with a revenue of Rs. 2,21,112 crore in FY24. Their net profit last year was Rs. 13,059 crore, which gave them that Rs. 99 EPS.

Adding Rs. 360 crore annually from this Qatar deal is like a decent 2.75% addition to its existing profits. We must remember that L&T is a majorly an Engineering & construction company. A majority of their revenues & profits come from here. So, to even reach to an EPS of Rs.99 per share, each year they have to work hard to get new construction orders and then execute it. By the way, over the last 5-years, their EPS has grown from Rs.68 levels to Rs.99 levels (a growth rate of 7.8% per annum).

Other Fundamentals of L&T

L&T’s balance sheet shows they’re sitting on Rs. 3,39,553 crore in total assets, with a debt of Rs. 1,13,089 crore.

They’re not strapped for cash either, cash flow from operations was Rs. 23,970 crore in FY24.

This Qatar project fits right into their core business, and with their financial muscle, they can handle it without any problems.

Plus, a contract this size boosts their order book, which was already at Rs. 4,70,000 crore last year. More orders mean more stability, and that’s gold for investors.

Conclusion

So, what do I think?

This isn’t just about Rs. 15,000 crore or a few extra rupees in EPS. It’s about L&T proving they’re a global heavyweight.

Winning a deal like this from QatarEnergy, a world leader in LNG, puts L&T (and India as a whole) on the world map in a big way.

For L&T, it’s new project will be a steady stream of revenue through 2030 (if things go as planned). It could cushion them against ups and downs in other sectors like infrastructure or real estate back home (if any).

Will the stock market cheer? Investors love big orders. But I have written this blog post to let my readers see beyond the hype and take an informed decision.

If L&T keeps its execution on point (and they usually do), that Rs. 2.62 EPS boost could compound with other projects, pushing their share price higher over time. Could we see their EPS cross Rs. 150 by 2030? I’d say it’s not out of the question. If the EPS continue to grow at about 7.5% each year, EPS of Rs.140 per share is a possibility. But I expect a slightly faster growth of L&T in years to come. Bagging Ultra-Mega projects like this helps get new more profitable orders.

What do you think about this new order of L&T (Larsen and Toubro)? I hope you liked my explanation of the project. Please tell me in the comments section below. It helps me to write more posts like this.

Have a happy investing.